What Churches Need to Know About RMD Donations to Charity

Benjamin Franklin once said “In this world, nothing can be said to be certain, except death and taxes.” Will Rogers added, “The only difference between death and taxes is that death doesn’t get worse every time Congress meets.”

But what if I told you that these three: death, taxes, and congress, could combine to make a win-win situation for your church and your congregation?

I’m referring to Qualified Charitable Distributions made possible by the Protecting Americans from Tax Hikes Act (PATH), and more specifically, the rules and regulations surrounding Required Minimum Distribution from IRA retirement accounts.

That’s a lot of big words and government terms, so let me explain...

Definitions: RMD vs QCD

I want to preface this by saying I am not a tax professional, so these definitions will be as close to layman’s terms as I can get.

What Is an RMD?

A Required Minimum Distribution (RMD) refers to the minimum amount you are required to withdraw from your retirement account(s) each year.

Depending on your birth year, the Internal Revenue Service (IRS) requires a certain percentage of retirement accounts to be dispersed each year, with most required to take a withdrawal once they reach age 70½ years old. The idea behind an annual RMD is simple: the government doesn’t want simple IRAs, Roth IRAs, or traditional IRAs to be used as inheritance funds, so they now require distribution based on life expectancy.

The government enforces this with an excise tax, which means if the normal distribution is not made, the IRS takes a 25% fee. The problem is those distributions must be made in cash; they cannot be rolled over into another fund tax-free so will increase the owner’s taxable income for the year and create a greater tax burden.

To put it as simply as possible, this money is coming by government order, there is no way to roll over or avoid it without penalty, and your member is going to need to do something about it if they want to be tax savvy.

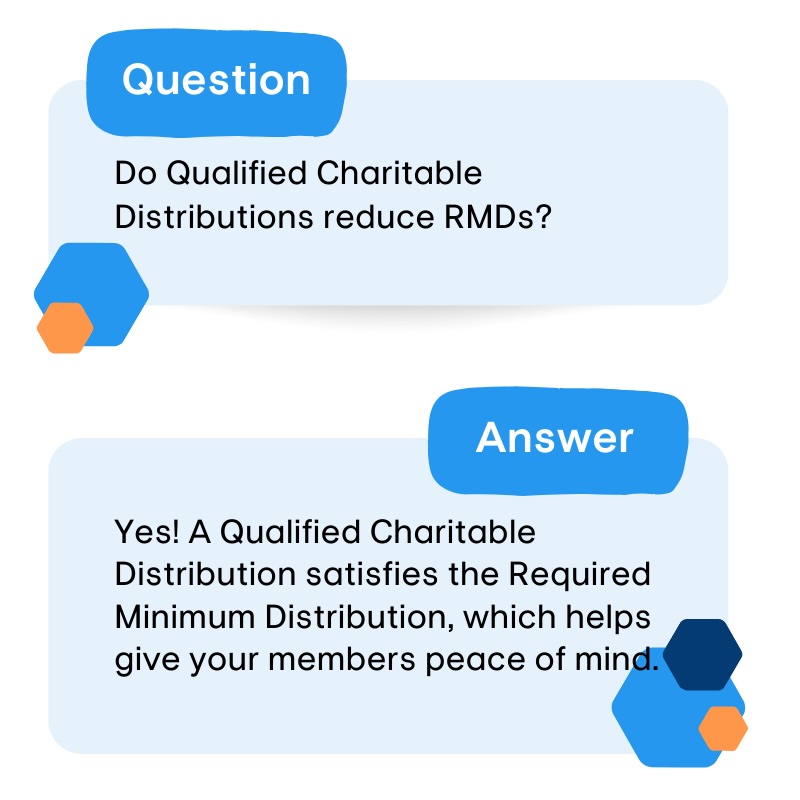

Do QCDs Reduce RMDs?

Here is where the Protecting Americans from Tax Hikes Act (PATH) steps in.

PATH renewed or created many tax breaks for Americans in 2015, including charitable gift contributions (Congress renewed this act in 2022). This act codified the practice of charitable giving directly from IRA retirement accounts, called Qualified Charitable Distributions (QCD).

You probably noticed that RMD and QCD both share the word “distributions” and that is intentional. Yes, QCDs can satisfy RMDs!

So let’s get into the win-win situation I was talking about before...

Win #1: QCDs Are Great for Church Members

There is probably a large group of hard-working members aged 55-65 who are considering retirement soon in your congregation right now.

They’ve worked all their life, saved and sacrificed to provide for their family, and now a large life change is approaching. Hopefully, they’ve spoken to a tax advisor for advice, and even more importantly, I hope they’re speaking with their church leadership for Godly guidance.

Here is an opportunity for you to counsel them and maybe relieve some of their fears.

The money in these IRAs has been growing for decades, has gone up and down with the economy, and every single book/podcast/seminar your member has listened to has screamed “DON’T TOUCH THE MONEY” to them repeatedly. But now, they have to.

How Qualified Charitable Distributions Benefit Your Members

By providing an avenue for a Qualified Charitable Distribution, your church can provide an eligible charity for the RMD and your member can avoid increased taxes on Social Security, and increased Medicare premiums, and can still take advantage of any other tax deductions or tax bracket they may be utilizing each year as the QCD is not treated as ordinary income and is exempt from income taxes; distributions are generally tax-free.

They may even be able to continue taking the standard deduction on their tax return in that tax year!

QCDs Bring Peace of Mind

This can bring real peace of mind to your members, in addition to getting them more involved in giving to ministry and the eternal benefits that come with it.

Your church also most likely has members already receiving IRA distributions as these members are in the 70-80 age range. If these members are utilizing tax benefits, their tax advisor is already donating these RMDs to charities and other charitable organizations. Your congregation may not know a QCD can be made to their church home instead.

Don’t assume that just because a member may be donating their QCD to another charity, they wouldn’t want to change that starting in 2025 to further God’s work. They may just need to be educated on the opportunity. What a blessing they could be overlooking!

Watch our video below on how to ask members to donate (without really asking them) to learn more about how to encourage IRA owners to leverage the RMD and charitable contributions for your church:

Make IRA RMD Charitable Donations Part of Your Fundraising Strategy

This could also apply to potential donors outside of your congregation as well. Letting your community know you are a positive force in the area and a gracious steward of resources could attract potential IRA custodians to further God’s Kingdom without even intentionally doing so, and hopefully create opportunities for relationship building and gospel invitations.

These IRA owners already give to charity, so why not let their charitable giving strategy include your ministry?

Win #2: QCDs Are Great for Your Ministry

This one is self-explanatory: Your church gets a charitable donation to further the ministry.

But keep reading to learn more about the ins and outs of QCD donations to churches.

QCD Donations to Church Can Be Huge

Additionally, the charitable contributions from RMD are not a small amount and can be a huge boon to your ministry.

For instance, a current imaginary member of your church, age 73, with $100,000 in a taxable IRA beginning in 2023 would need to accept a distribution this year of around $3,700. It is not uncommon for individuals to have ten times that amount in their IRA account, in addition to the already received Social Security payments and Medicare benefits, or any other savings funds they might be using such as a 401k or Roth IRA.

These members need to do something with the funds to avoid a higher tax bracket for their adjusted gross income, why not donate a portion or full amount to your ministry in the form of a QCD?

This could be an opportunity to partner with your members in taking on new missionaries, expanding church operations, or maybe even paying down some of the debt holding back your ministry. And if you are using ChurchTrac Accounting, you will easily see where exactly in your budget this money could be put to good use.

The Limits of Qualified Charitable Donations

Keep in mind, that charitable contributions from IRAs are limited to $100,000 per donor, per year, and $200,000 for married couples filing jointly, so while there are some limitations to the amount of the QCD, the potential results are still impressive. For further help, view the RMD Calculator to determine the amount of the potential RMD.

IRS Laws and Regulations for QCDs

The QCD is not treated as gross income for your member, so they would not use this as a tax deduction, though there are still ways for them to use this on their taxes even if they do not itemize. Your church may benefit from speaking with a tax advisor to ensure all of your processes are current with current IRS laws and regulations and your local state tax rules.

RMD Contributions to Charity Will Bless Your Church

Donating an RMD through a QCD from an IRA by the PATH is a great idea. Hopefully, you now have a better understanding of what all those letters mean, and what a QCD may do for your ministry and your people.

If you are looking for ways to bring up the subject of making qualified charitable distributions to your people, I recommend checking out our previous articles on giving, especially our video “How to Ask People to Give (Without Asking).” Illustrations, giving testimonies, and even having a certified tax accountant come to give a seminar to your people could be helpful.

Ultimately, it is up to you and your leadership to decide if this is something you want to pursue, and I pray that God blesses and guides your decisions.