1099 VS W2: A Guide For Churches

Key Takeaways

- W-2 workers are employees who operate under the church’s direction and oversight, while 1099 workers are independent contractors who control how their work is done.

- Most pastors and regular church staff should be paid as W-2 employees.

- Misclassification can result in back taxes and penalties, so when there’s uncertainty, choosing W-2 or seeking professional guidance is usually the safest path.

Churches depend on a wide range of people to carry out ministry: pastors, administrative staff, worship leaders, guest speakers, and outside service providers. Somewhere along the way, almost every church asks the same question: Should this person be paid as a 1099 contractor or a W-2 employee?

It’s an understandable question, especially for churches trying to be good stewards of limited resources. But the difference between a church 1099 and a church W-2 isn’t just a technical detail. Classifying workers incorrectly can lead to tax issues, penalties, and frankly, avoidable stress.

This guide is designed to help churches understand the difference between church 1099 and church W-2 workers, why the distinction matters, and how to make the right decision with confidence.

My Experience: Why Churches Get This Wrong

Working with churches, we’ve seen this confusion come up again and again, and it’s rarely intentional. Ministry is busy, teams are stretched thin, and financial decisions are often made quickly.

Common reasons churches default to 1099 include:

- “They’re only part-time.”

- “They only work on Sundays.”

- “They’re helping us out temporarily.”

- “It’s simpler than running payroll.”

The problem is that none of those factors determines whether someone should be paid as a 1099 or a W-2. The IRS focuses on the nature of the relationship, not the church’s intent or convenience.

For most churches, this situation usually doesn’t start as a financial decision at all; it starts as a people decision. A church is in transition, a role needs to be covered, or someone trustworthy steps up and says they’re willing to help. Maybe it’s a worship leader filling in “for a season,” or a children’s worker helping while volunteers are being rebuilt.

At first, it feels temporary. Leadership tells themselves they’ll reassess later. Payroll feels like overkill for something that might only last a few months, so the church pays the person as a 1099 to keep things moving. Ministry continues, Sundays come and go, and before anyone realizes it, that “short-term” role has quietly turned into six months… or a year.

This is where frustration usually sets in. Church leaders are surprised to learn that part-time hours, Sunday-only schedules, or “temporary” arrangements don’t determine whether someone should receive a 1099 or a W-2. What matters is the relationship itself. The IRS looks at who controls the work and how integrated that role is into the church, not whether the arrangement felt informal or convenient at the time.

Most churches don’t get this wrong because they’re careless. They get it wrong because ministry moves faster than paperwork, and the classification question often doesn’t feel urgent until it suddenly is.

What’s the Difference Between 1099 and W-2?

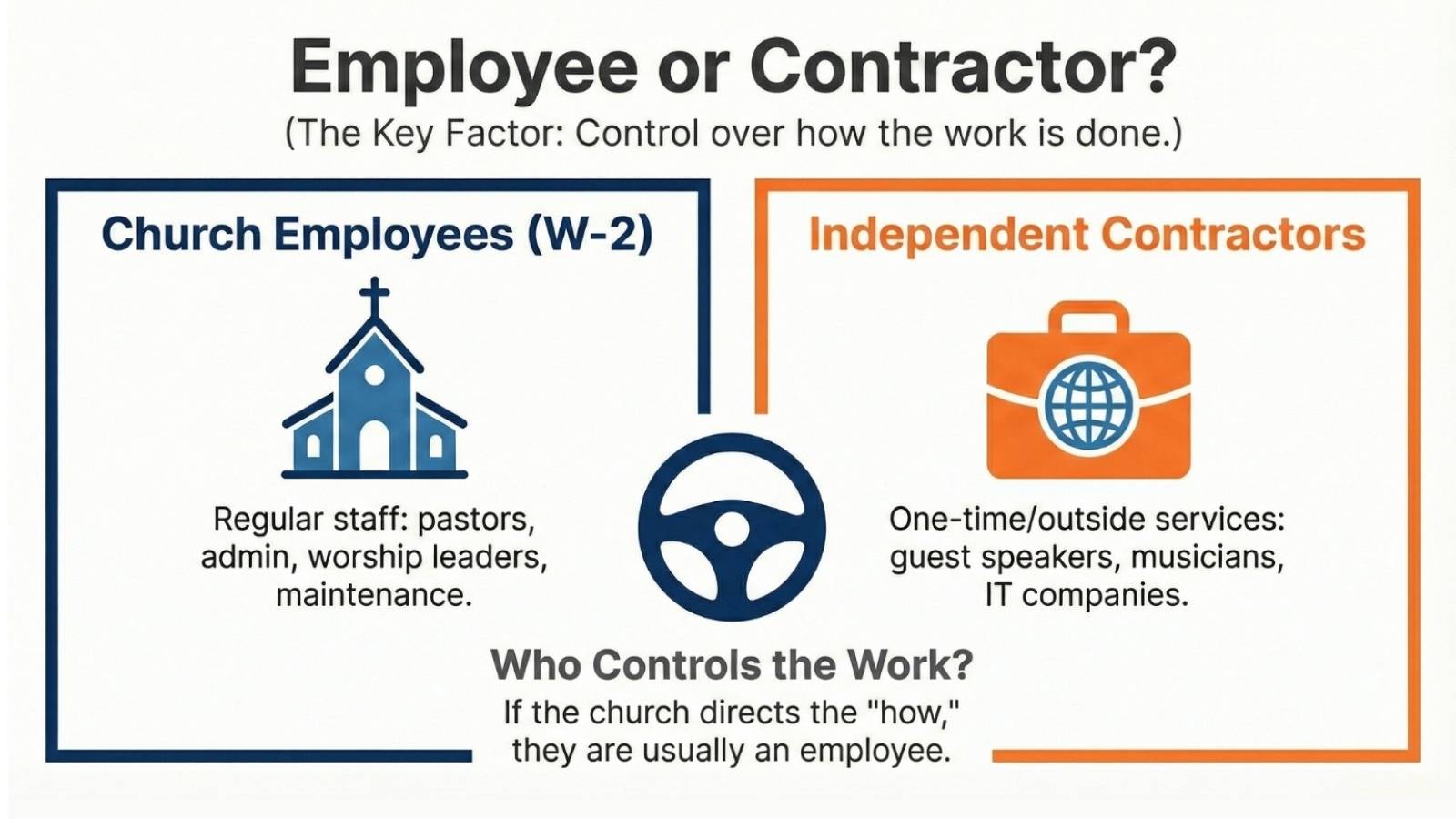

The core difference between a W-2 employee and a 1099 contractor comes down to control.

A W-2 employee is someone whose work is directed by the church. The church sets expectations, provides oversight, and determines how the role functions within ministry operations. This typically includes regular staff members who serve ongoing roles in the church.

A 1099 contractor, on the other hand, operates independently. The church may define the outcome of the work, but not the process. Contractors typically offer their services to multiple clients, use their own tools or methods, and are engaged for specific projects or services rather than ongoing ministry roles.

Who Is Usually W-2 vs 1099?

In most churches, roles like pastors, administrative staff, worship leaders under church direction, children’s ministry workers, and regular maintenance staff are considered employees and should be paid using a W-2.

Independent contractors are more commonly found in situations involving outside or one-time services. Examples may include a guest speaker invited for a single event, a musician hired for a special service, or an outside company providing bookkeeping, IT, or cleaning services. In these cases, the key factor is whether the individual or business maintains control over how the work is done.

Why Misclassification Is a Big Deal for Churches

Misclassifying workers can create serious problems, even for churches acting in good faith. The Internal Revenue Service may require churches to pay back payroll taxes, penalties, and interest if a worker is incorrectly classified. In some cases, state labor laws may also come into play.

Beyond financial consequences, misclassification can impact a church’s credibility and distract leadership from ministry. What feels like a small decision upfront can turn into a significant administrative burden later.

What Churches Should Do Before Choosing

Before deciding how to pay someone, it’s important for churches to pause and look beyond the immediate need being filled. The question isn’t simply what work is being done, but how the relationship actually functions. Taking a little extra time upfront can prevent significant cleanup later.

Start by evaluating who has control over the work. If the church sets the schedule, defines responsibilities, provides direction, or expects the person to follow established ministry processes, that points toward a W-2 employee. Even when a role is part-time or limited to certain days, regular oversight and integration into church operations matter more than the number of hours worked.

Next, consider whether the role is ongoing or truly project-based. A role that continues week after week, especially one that is essential to regular church functions, is rarely a good fit for a 1099 arrangement. Independent contractors are typically engaged for specific outcomes or short-term services, not for open-ended ministry roles that evolve over time.

It’s also helpful to look at the individual’s broader work situation. Someone who offers similar services to multiple organizations, advertises those services independently, and supplies their own tools or methods is more likely to qualify as a contractor. On the other hand, someone who serves only the church and functions as part of the internal team is usually an employee, even if the arrangement feels informal.

Pro Tip: Clear documentation plays an important role as well. Written agreements can help define expectations when working with independent contractors, but it’s important to remember that a contract alone doesn’t determine classification. The day-to-day reality of the relationship must align with what’s on paper.

When in Doubt, Reach Out

Choosing between a church 1099 and a church W-2 usually isn’t a philosophical debate; it’s a “we need to pay this person” moment. And when things are busy, it’s tempting to choose whatever feels fastest and move on. The problem is that those decisions have a way of resurfacing later, usually at the least convenient time (like year-end reporting or tax season).

Taking a little extra time to classify workers correctly is one of those behind-the-scenes decisions that most people will never notice when it’s done right, but everyone feels it when it’s done wrong. It protects the church, sets clear expectations for the person being paid, and saves leadership from uncomfortable cleanup conversations down the road.

FAQs: 1099 vs W-2 for Churches

Can a church pay a pastor with a 1099?

In almost all cases, no. Pastors are generally considered employees for income tax purposes and should receive a W-2.

Do part-time or Sunday-only workers qualify as 1099 contractors?

Not necessarily. Hours worked or schedule alone do not determine classification.

Can a church change someone from 1099 to W-2 later?

Yes, but it should be done carefully and may require reviewing prior payments.

Do churches have to issue 1099 forms?

Yes. If a church pays a qualifying independent contractor over the IRS reporting threshold, a 1099-NEC is required.

What if a church has misclassified someone in the past?

Many churches discover this later. In those situations, it’s wise to consult a tax professional to determine the best corrective path.

Financial Disclaimer: This article is provided for informational purposes only and does not constitute professional accounting, tax, or financial advice. Church tax laws are complex and subject to change based on federal, state, and denominational regulations. ChurchTrac is a software provider, not a CPA firm. We strongly recommend consulting with a qualified tax professional or certified public accountant before making financial decisions or filing tax-related documents for your ministry.