Clergy Housing Allowance 101

Your pastor might be losing thousands of dollars in take-home pay every year—and the IRS is perfectly happy to let you keep making this classic mistake.

The clergy housing allowance is the most significant tax benefit available to ministers, yet it is often the most misunderstood. Handled correctly, it allows pastors to exclude housing-related expenses from federal income tax. Handled poorly, it’s a compliance landmine that leads to IRS audits and back taxes.

Key Takeaways: This article covers the essentials of Clergy Housing Allowance:

- What it is: A federal income tax exclusion for housing-related expenses.

- The Golden Rule: It must be officially designated by the church board in advance and in writing.

- The Tax Impact: It reduces federal income tax but remains subject to SECA (Self-Employment Contributions Act) taxes.

- The Catch: It is limited to the lesser of the designated amount, actual expenses, or the fair rental value of the home.

What Is Clergy Housing Allowance?

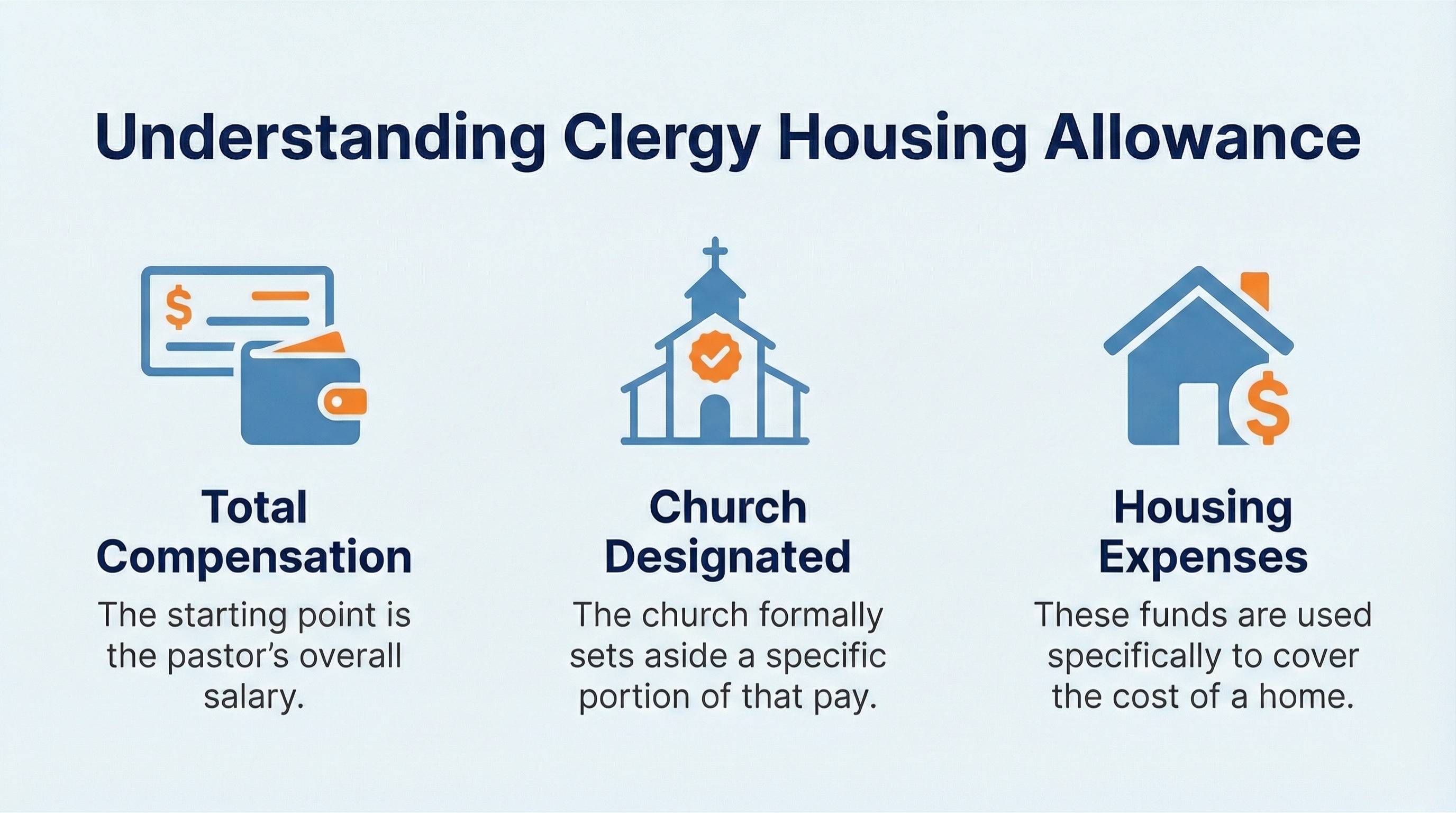

A clergy housing allowance is a portion of a pastor’s compensation that a church designates to help cover housing expenses.

Under IRS rules, eligible ministers may exclude this amount from federal income tax, provided it is designated in advance and used for qualifying housing costs.

This benefit is unique to clergy and does not function like a standard employee housing benefit. Although it is commonly referred to as a pastor or clergy housing allowance, the IRS uses the broader term “housing allowance for ministers,” and the same rules apply regardless of wording.

What Expenses Can Be Covered

The clergy housing allowance may be used for a wide range of housing-related expenses. These typically include rent or mortgage payments, utilities such as electricity, gas, water, and internet, furnishings and appliances, repairs and maintenance, and homeowners or renters insurance.

The allowance is intended to cover the cost of providing and maintaining a home. It does not extend to unrelated personal expenses, which is why pastors should track actual housing costs throughout the year.

How the Clergy Housing Allowance Is Designated

A key requirement of the clergy housing allowance is that it must be designated in advance.

This means the church must formally approve the allowance before the compensation is paid. Churches usually do this through board or committee minutes, an annual budget, or a written compensation agreement.

Retroactive designations are not allowed, which is why churches are encouraged to review and approve housing allowances before the start of each year or before a pastor begins receiving compensation.

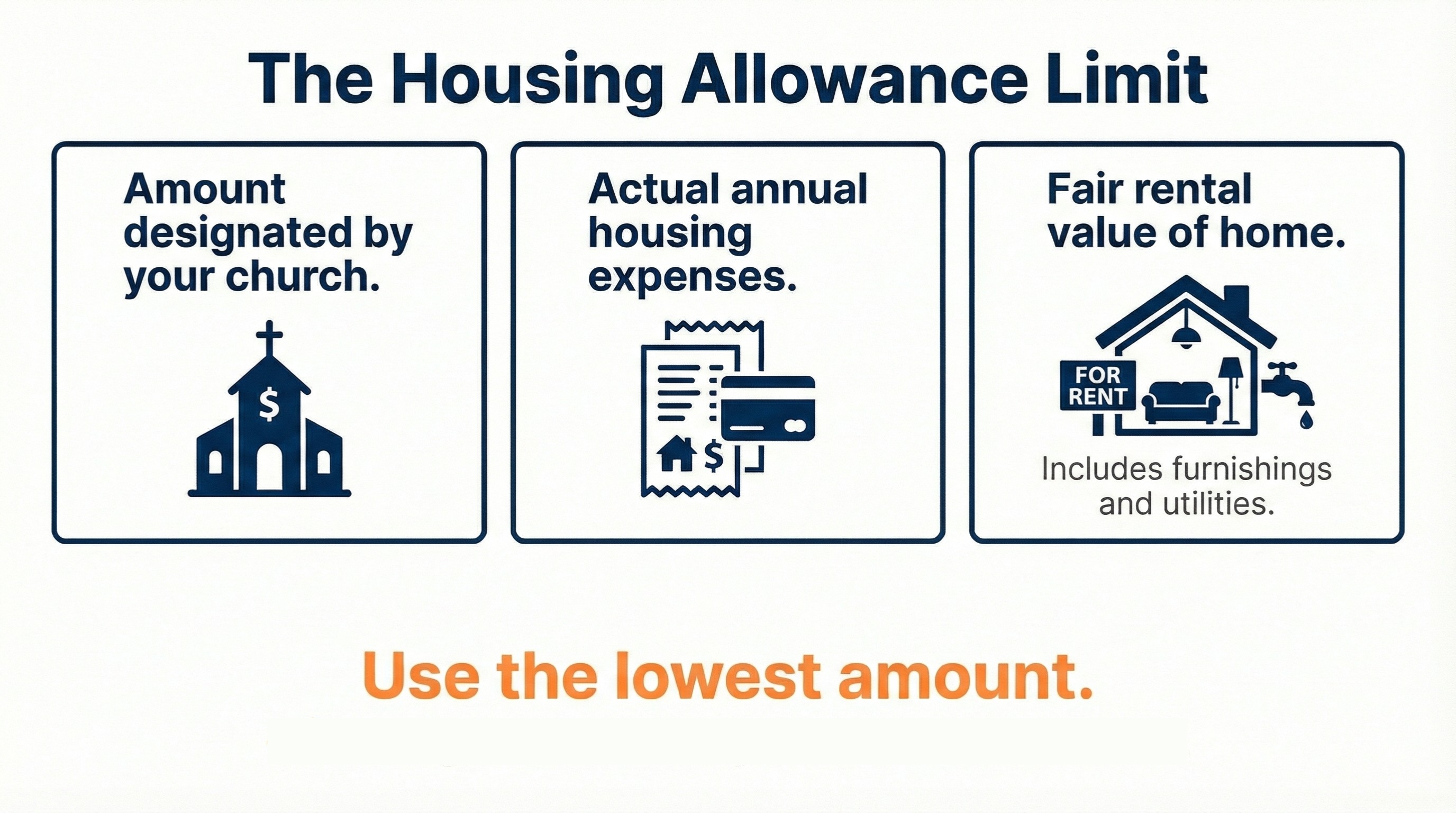

How Much Can Be Designated

The amount of a pastor's housing allowance is limited by three factors:

- First, it cannot exceed the amount designated by the church.

- Second, it cannot be more than the pastor’s actual housing expenses for the year.

- Third, it cannot exceed the fair rental value of the home, including furnishings and utilities.

The lowest of these three amounts determines how much may be excluded from federal income tax. This is why realistic estimates and periodic review are important.

Housing Allowance and Taxes: What Pastors Need to Know

Although the clergy housing allowance may be excluded from federal income tax, it is still subject to self-employment tax.

Ministers are treated as self-employed for Social Security and Medicare purposes, which means housing allowance amounts are included when calculating self-employment tax.

This distinction often surprises pastors and is a common source of confusion, making education and clear communication especially important.

Check out our article The #1 Pastor Payroll Mistake (It's FICA) ›

Reporting the Pastor Housing Allowance

When properly designated, the pastor housing allowance is generally not included in Box 1 of the pastor’s W-2.

However, pastors are still responsible for determining how much of the allowance qualifies for exclusion when filing their personal tax return.

Any portion that exceeds actual expenses or fair rental value must be reported as taxable income.

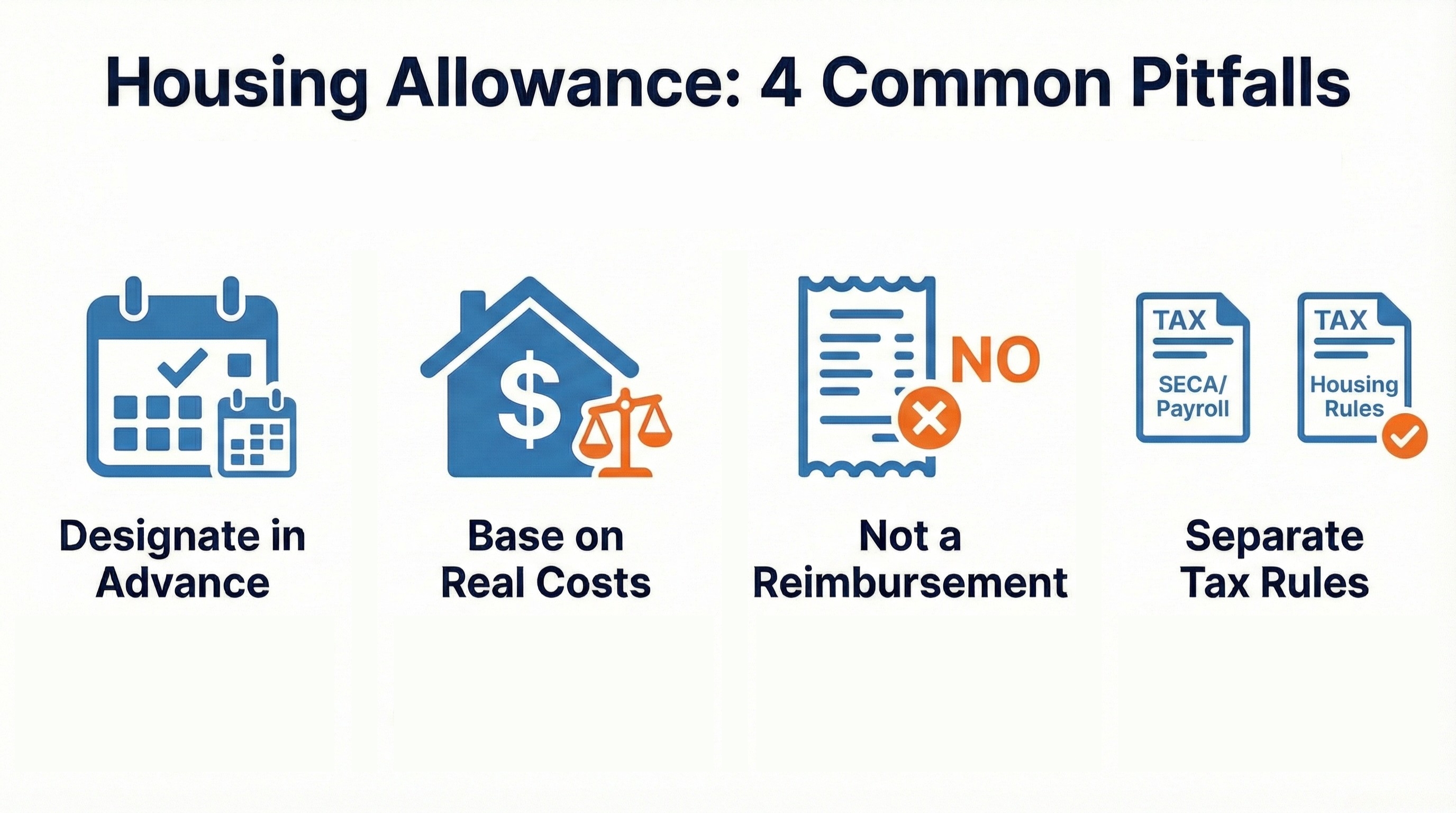

Common Clergy Housing Allowance Mistakes

Most housing allowance problems come from a few recurring mistakes.

- These include failing to designate the allowance in advance

- Designating an amount without considering actual housing costs or fair rental value

- Treating the allowance like a reimbursement plan

- Confusing housing allowance rules with payroll taxes or SECA allowances

These issues are usually preventable with simple planning and documentation.

Final Thoughts on Housing Allowance for Ministers

Churches should review housing allowances annually and adjust them when a pastor’s housing situation changes. Keeping documentation simple and consistent helps avoid confusion later.

Because clergy tax rules are unique, many churches benefit from working with a CPA or tax professional familiar with minister compensation. A little proactive effort now can prevent bigger problems down the road.

FAQs: Clergy Housing Allowance

Can a pastor change their housing allowance during the year?

Yes. A pastor housing allowance can be changed during the year, but only on a prospective basis. Any change must be formally approved and documented before future payments are made.

What happens if a pastor doesn’t use the full housing allowance?

If actual housing expenses are less than the designated allowance, the unused portion becomes taxable income and must be reported accordingly.

Is the clergy housing allowance subject to Social Security tax?

Yes. Housing allowance amounts are subject to self-employment tax, even though they may be excluded from federal income tax.

Can retired clergy receive a housing allowance?

In some cases, retired clergy may still receive a housing allowance if it is properly designated and the individual qualifies under IRS guidelines.

Does every pastor qualify for a housing allowance?

No. Only individuals who meet the IRS definition of a minister for tax purposes are eligible for a clergy housing allowance.

Financial Disclaimer:This article is provided for informational purposes only and does not constitute professional accounting, tax, or financial advice. Church tax laws are complex and subject to change based on federal, state, and denominational regulations. ChurchTrac is a software provider, not a CPA firm. We strongly recommend consulting with a qualified tax professional or certified public accountant before making financial decisions or filing tax-related documents for your ministry.