The #1 Pastor Payroll Mistake (It's FICA)

Key Takeaways

- Pastors are treated differently from other church employees when it comes to Social Security.

- While most employees fall under FICA, pastors pay Social Security through SECA, which means churches cannot pay or match the employer portion of Social Security on their behalf.

January 1st is often a hopeful moment for small churches. Payroll gets updated, numbers are changed, and things move forward.

Unfortunately, this is also when one of the most common pastor payroll mistakes quietly happens.

A well-meaning church treasurer runs the pastor's pay the same way they run everyone else’s payroll. Without realizing it, the church begins paying the employer’s share of Social Security—something the IRS does not allow for pastors.

The good news is that it’s fixable once you understand why pastor payroll is different.

Should Churches Pay the Employer’s Share of FICA?

In a typical payroll setup, an employer pays half of an employee’s Social Security and Medicare taxes, while the employee pays the other half. Because pastors receive a W-2 and are treated as employees in many ways, it’s natural to assume the same rules apply. Learn more about W-2s vs 1099s ›

But they don’t.

When a church pays the employer portion of Social Security for a pastor, it creates a compliance issue. The compliance issue is this:

Churches are not legally allowed to pay the employer portion of Social Security and Medicare taxes for a pastor.

Under federal tax law, ministers are treated as self-employed for Social Security and Medicare purposes, even though they receive a W-2 and are employees for income tax reporting.

That means:

- The pastor is responsible for 100% of Social Security and Medicare taxes through the Self-Employment Contributions Act (SECA).

- The church must not pay or match the employer portion, like it would for a non-minister employee.

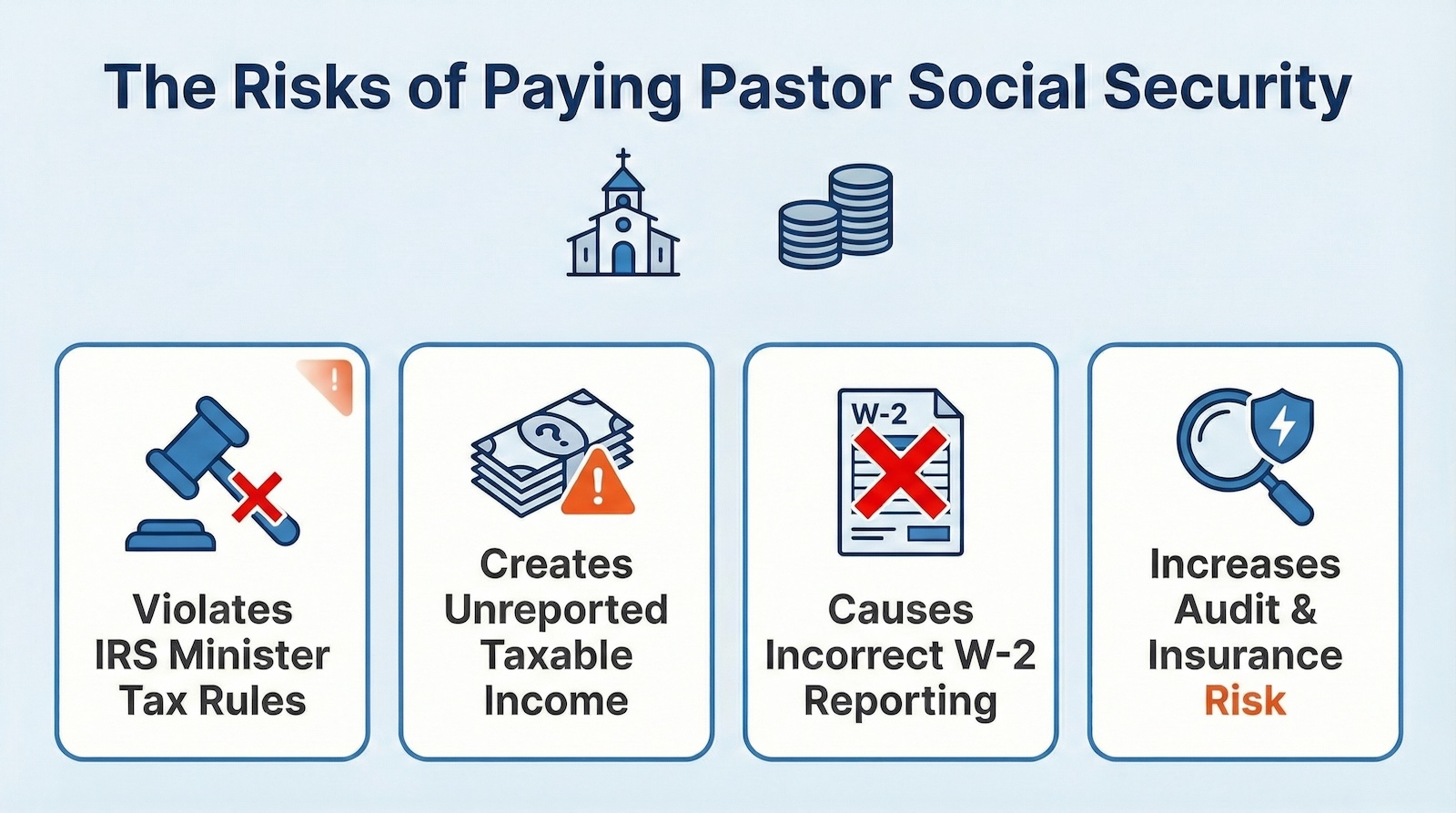

When a church does pay the employer share of Social Security or Medicare for a pastor, it creates problems, such as:

- Violates IRS minister tax rules

- Creates taxable income that often goes unreported

- Results in incorrect payroll and W-2 reporting

- Increases audit and insurance risk

This mistake commonly happens during pay raises, leadership changes, or when payroll is set up like a standard W-2 employee, but it is not compliant.

What does the IRS Require for Pastor Social Security?

Pastors have a unique dual tax status. For income tax purposes, they are considered employees. For Social Security and Medicare, however, they are treated as self-employed.

The IRS classifies pastors as self-employed for Social Security and Medicare purposes because of the unique nature of ministry and how clergy have historically been treated under federal law.

Why Are Pastors Treated as Self-Employed for Social Security and Medicare?

Under the tax code, ministers are viewed as having a dual role:

- They serve a church (which looks like employment for income tax purposes)

- But they also function as individuals exercising an ordained calling, not a traditional employer-controlled position.

Because of this, the IRS places pastors under the Self-Employment Contributions Act (SECA) instead of the standard employee FICA system.

This structure allows ministers to:

- Remain eligible for Social Security benefits

- Pay into the system directly, rather than through employer withholding

- Maintain consistency across denominations and church structures, regardless of size or governance

What this means:

This means the church does not withhold Social Security taxes from a pastor’s paycheck and does not pay or match those taxes. Instead, pastors pay Social Security through the Self-Employment Contributions Act, commonly referred to as SECA.

What is a SECA Allowance?

A SECA allowance is additional taxable compensation designed to help offset the pastor’s Social Security responsibility.

It allows the church to support the pastor financially without directly paying Social Security taxes on their behalf.

It’s important to understand that a SECA allowance is not tax-free, not a reimbursement, and not employer-paid FICA. When structured correctly, however, it keeps the church compliant while still providing meaningful support.

How To Fix Your Clergy Payroll Mistakes

Correcting clergy payroll mistakes does not have to be complicated or stressful. In most cases, it simply requires adjusting how payroll is handled going forward. Here are the things to look for:

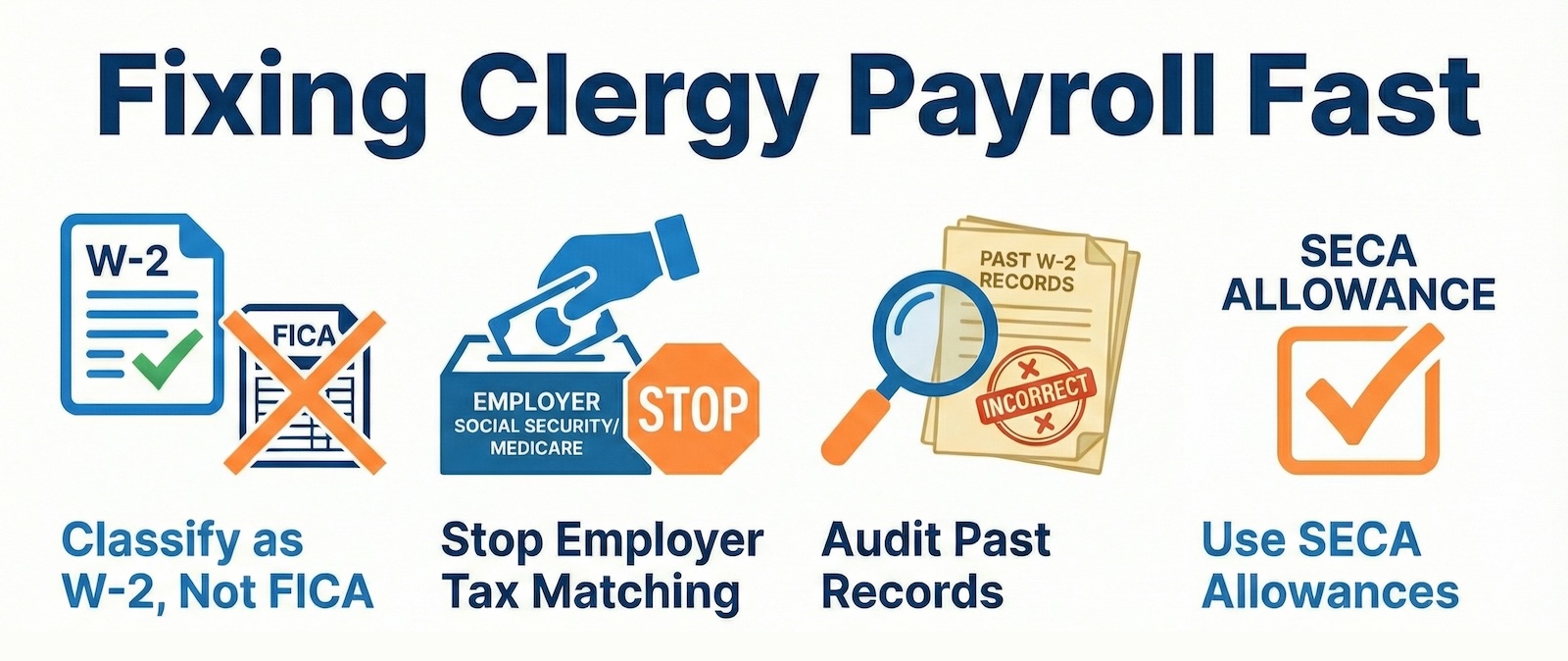

- Review how the pastor is classified in payroll: Confirm the pastor is set up as a W-2 employee for income tax purposes, but not subject to Social Security or Medicare withholding. Payroll software often defaults to standard employee settings, so this is an important first check.

- Stop any employer-paid Social Security or Medicare contributions: If the church is currently paying or “matching” the employer portion of Social Security, this should be discontinued immediately. Churches are not permitted to pay FICA taxes on behalf of ministers.

- Check prior pay records and W-2 reporting: Look for Social Security or Medicare amounts that may have been incorrectly paid or reported in the past. While many churches simply correct the issue going forward, some situations may require guidance from a tax professional.

- Consider a SECA allowance instead: If the church wants to help offset the pastor’s tax burden, a SECA allowance can be provided as additional taxable compensation. This allows the church to support the pastor without violating IRS rules.

How Churches Apply for SECA?

A SECA allowance is a church decision, not a tax election made with the IRS. In other words, pastors do not apply for a SECA allowance on their tax return—the church chooses whether to offer one as part of its compensation structure.

Applying a SECA allowance is typically straightforward:

- Decide whether the church will offer a SECA allowance and determine the amount (often based on budget and compensation philosophy).

- Formally designate the allowance in writing (such as in board minutes or a compensation agreement).

- Include the allowance as taxable compensation for income tax purposes (it is not exempt from income tax).

- Ensure the allowance is not treated as an employer-paid FICA tax or run through payroll as such.

Because every church’s situation is different, churches may want to consult a CPA or tax professional familiar with church payroll and minister taxation. But in most cases, this adjustment can be made quickly and cleanly—often within the same month it’s identified.

Pastor Pay, FICA, and SECA

At a high level, most employees fall under FICA, while pastors fall under SECA for Social Security purposes. This distinction affects how taxes are paid, not how much a church values or supports its pastor.

When churches understand this difference, they can budget more accurately, stay compliant with IRS rules, and avoid difficult corrections down the road.

FAQS: Pastor Payroll Mistake

Can a church pay the pastor’s Social Security for them?

No. Churches cannot pay or match Social Security taxes for pastors as they do for non-minister employees.

Is a SECA allowance required?

No. It’s optional, but many churches use it to help offset the pastor’s Social Security obligation.

Is a SECA allowance tax-free?

No. SECA allowances are taxable income.

Can we reimburse the pastor for SECA taxes instead?

No. Reimbursements are still considered taxable compensation and do not resolve the compliance issue.

Does this affect housing allowance?

No. Housing allowance is separate, though SECA still applies to eligible housing allowance amounts.

What if we’ve been doing this wrong for years?

You’re not alone. Most churches discover this unintentionally. The best step is to correct it going forward and consult a CPA or payroll professional familiar with church payroll.

Financial Disclaimer: This article is provided for informational purposes only and does not constitute professional accounting, tax, or financial advice. Church tax laws are complex and subject to change based on federal, state, and denominational regulations. ChurchTrac is a software provider, not a CPA firm. We strongly recommend consulting with a qualified tax professional or certified public accountant before making financial decisions or filing tax-related documents for your ministry.