How to Pay Church Interns (W-2 vs 1099 vs Scholarship)

Key Takeaways

This guide breaks down how to pay church interns legally and correctly, explains the differences between W-2 vs 1099 vs scholarship payments, and walks through when (and if) each option applies.

Most church interns should be paid as W-2 employees. Interns rarely qualify as 1099 contractors, and scholarships can only be used in very limited, education-specific situations. Paying interns incorrectly can result in IRS penalties, back taxes, and labor law violations.

But when it comes time to pay interns, many churches pause and ask the same question:

Should church interns be paid as W-2 employees, 1099 contractors, or through scholarships or stipends?

What Does the IRS Consider a Church Intern?

Despite the common use of the term intern, the IRS does not recognize “intern” as a special tax classification. From a legal and tax standpoint, interns are evaluated the same way as any other worker.

The key question is how the work is performed.

If the church:

-

Sets the intern’s schedule

-

Assigns ministry responsibilities

-

Supervises daily tasks

-

Provides training and direction

Then the intern is almost always considered an employee, regardless of age, duration, or part-time status.

Paying Church Interns as W-2 Employees (Most Common Option)

If you’re unsure how churches should handle worker classification overall, this guide walks through the differences clearly: 1099 vs. W-2: A Guide for Churches.

For most churches, paying interns as W-2 employees is the correct and safest choice.

When a W-2 Is Required

A W-2 is generally required when:

-

The intern works regular or scheduled hours

-

The church directs how the work is done

-

The intern represents the church publicly

-

Compensation is tied to ministry duties

-

The internship lasts more than a brief, one-time project

In other words, if the intern functions as part of your ministry team, they are likely an employee.

Paying Church Interns as 1099 Contractors (Usually Incorrect)

Many churches are tempted to pay interns as 1099 independent contractors to avoid payroll taxes or simplify setup. Unfortunately, this is one of the most common (and risky) mistakes.

Why Interns Rarely Qualify as Contractors

Independent contractors:

-

Control how their work is done

-

Set their own schedules

-

Offer services to multiple clients

-

Operate independently from the organization

Most church interns do none of these things. They are trained, supervised, scheduled, and directed by the church, with clear indicators of employee status.

Paying Church Interns Through Scholarships or Stipends

Scholarships and stipends are often misunderstood when paying interns.

When Scholarships May Be Appropriate

Scholarships may apply only when:

-

The intern is enrolled in an accredited educational institution

-

Payments are tied to tuition or qualifying educational expenses

-

Funds are not compensation for services

-

Ministry work is not required in exchange for payment

In practice, most church internships do not qualify for true scholarship treatment.

W-2 vs 1099 vs Scholarship: Quick Comparison

| Factor | W-2 Employee | 1099 Contractor | Scholarship |

|---|---|---|---|

| Who controls the work | Church | Worker | Educational institution |

| Payroll tax handling | W-2 issued | 1099-NEC issued | No wage reporting |

| Common for interns | Yes | Rare | Limited |

| Compliance risk | Low | High | Medium |

| Appropriate use | Most interns | Independent vendors | Education-only aid |

Pro Tip: Interns who function as part of your ministry team should almost always be set up as W-2 employees to ensure accurate payroll, tax reporting, and long-term clarity.

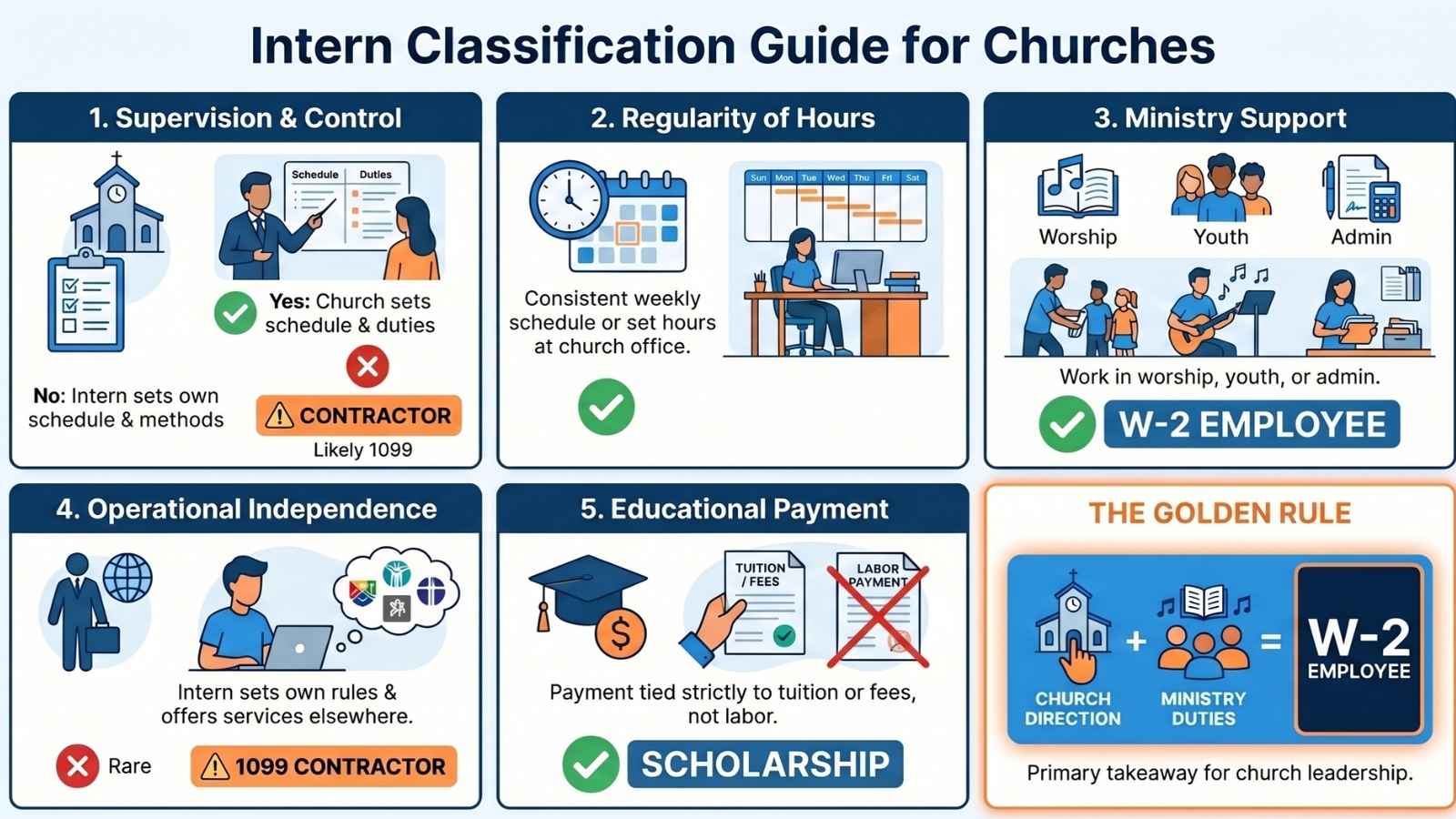

Decision Tree: Should This Church Intern Be Paid as W-2?

The graphic emphasizes that interns who work under church direction and perform ministry duties should almost always be classified as W-2 employees, with 1099 and scholarship options applying only in rare situations.

Start Here

1. Does the church control how the intern does their work?

(Schedule, duties, supervision, training, expectations)

-

✅ Yes → Go to next question

-

❌ No → Likely NOT an intern (possible contractor—evaluate carefully)

2. Does the intern work set or regular hours for the church?

-

✅ Yes → Go to next question

-

❌ No → Go to next question

3. Is the intern performing ministry-related work that supports church operations?

(Worship, youth, admin, outreach, tech, children’s ministry, etc.)

-

✅ Yes → W-2 EMPLOYEE

-

❌ No → Go to next question

4. Is the intern truly operating independently?

(Sets their own schedule, controls how work is done, offers services to others)

-

✅ Yes → POSSIBLY 1099 (rare for interns) ⚠️ → Go to next question

-

❌ No → W-2 EMPLOYEE

5. Is the payment tied strictly to education (not work)?

(Tuition, required fees, no compensation for services)

-

✅ Yes → SCHOLARSHIP (limited use) ⚠️

-

❌ No → W-2 EMPLOYEE

Golden Rule: If the intern works under church direction and performs ministry duties, they should almost always be paid as a W-2 employee.

When in Doubt, W-2 Is the Safest Path

Church internships are valuable, formative experiences, but they still involve real work. Ultimately, most interns function as employees and should be treated as such.

Financial Disclaimer: This article is provided for informational purposes only and does not constitute professional accounting, tax, or financial advice. Church tax laws are complex and subject to change based on federal, state, and denominational regulations. ChurchTrac is a software provider, not a CPA firm. We strongly recommend consulting with a qualified tax professional or certified public accountant before making financial decisions or filing tax-related documents for your ministry.

FAQs: Paying Church Interns

Only if no compensation is provided and the role truly qualifies as volunteer service. Once payment is involved, employment rules apply.

Generally, no. Most interns must be paid at least minimum wage unless a specific exemption applies.

Yes, but they must be clearly separated. Wages are taxable; qualified scholarships are not.

Yes, if they meet employee criteria, even for short-term roles.

Corrections are possible, but it’s best to address issues early. Consult a payroll or tax professional promptly.